Risk and Known Unknowns: Planning for What We Can’t Fully Predict.

I wanted to provide you with an update on markets, your portfolio, and our current strategic thinking. The year began constructively. During January and February, our portfolio experienced strong price appreciation, particularly due to our positioning in small banks and energy stocks, both of which benefited from improving earnings expectations and higher commodity prices. During this period, markets also appeared largely willing to look past geopolitical tensions surrounding Venezuela.

However, since February 28, 2026, when missiles and bombs began flying in the conflict involving Iran, market sentiment has shifted. Foreign equities have declined roughly 5%, while the S&P 500 has fallen approximately 1%. While the price movement itself has been modest, the nature of the risk environment has changed.

At this stage, the most significant risk facing markets is not what we know, it is what we know we cannot yet quantify. This concept is captured in what strategists often call the “known unknowns”: Risks that we are aware of but cannot model with precision. Examples include the potential economic effects of a widening regional conflict, supply disruptions in energy markets, and the possibility that war-driven commodity inflation reignites price pressures globally.

A simple analogy may help illustrate the point. Imagine discovering termites in a home. The termites themselves represent a known unknown. You know there is damage underway, but you cannot yet quantify the full extent of the structural harm hidden behind the walls. In financial markets today, those “termites” are the reshuffling of global risk premiums caused by war, rising oil prices, and inflation expectations. Importantly, markets do not decline simply because risks exist. Markets decline when investors suddenly reprice those risks all at once.

Currently, we have not yet seen price capitulation, particularly in technology stocks and large passive index funds. If geopolitical escalation or sustained high oil prices begin to alter investor psychology, sentiment could change quickly. Under those conditions it would not be unusual to see a 20% equity correction, driven less by fundamentals and more by indiscriminate selling from individual investors. The market could stay down for quite some time due to poor market-driven technical factors and the Fed having to increase rates to fight unanticipated inflation.

This is where theory collides with reality. Academic finance assumes investors behave rationally and maintain diversified portfolios. In practice, markets are driven by human behavior, fear, greed, and herd dynamics. As the investor Howard Marks famously said: “You can’t predict. You can prepare.” That principle is central to our current strategy. Because we cannot precisely forecast the path of geopolitical events or investor sentiment, our responsibility is to manage risk before it becomes obvious to everyone else.

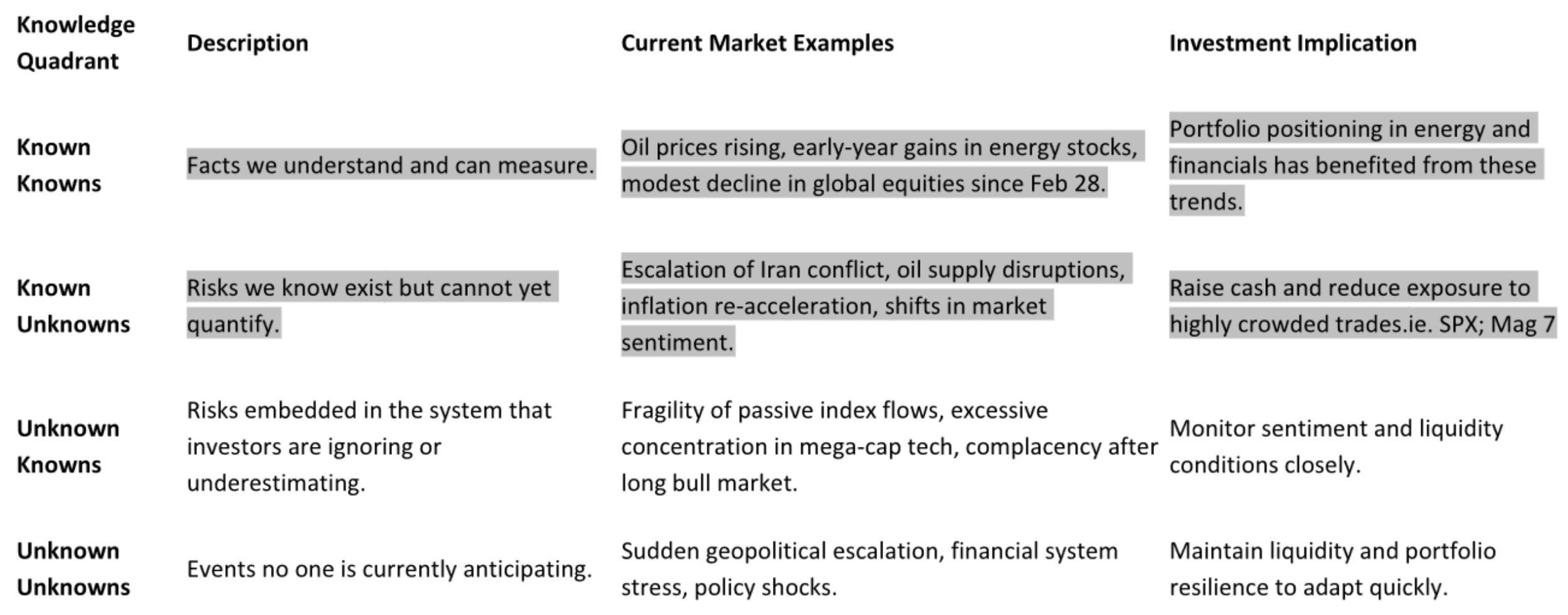

For this reason, we believe it is both prudent and disciplined to begin raising cash levels within the portfolio. Doing so allows us to: 1) Reduce downside exposure if volatility accelerates; 2) Preserve capital during potential drawdowns; 3) Maintain flexibility to deploy capital at more attractive valuations. Our goal is not to predict the next headline. Our goal is to ensure that your portfolio remains resilient regardless of what the next headline may be. In investing, preparation, not prediction, is the foundation of long-term success. Market Risk Framework Using the Rumsfeld Matrix Strategists often use a Rumsfeld Knowledge Matrix to classify uncertainty into four quadrants: known knowns, known unknowns, unknown knowns, and unknown unknowns.

Strategists often use a Rumsfeld Knowledge Matrix to classify uncertainty into four quadrants: known knowns, known unknowns, unknown knowns, and unknown unknowns.

Final Thoughts

Our objective remains unchanged: protect capital, manage risk, and compound wealth over time. Raising cash is not a prediction that markets will fall immediately. It is a recognition that the distribution of risk has widened, and disciplined investors prepare for that shift before panic forces everyone else to act. When uncertainty increases, discipline becomes even more important. By increasing cash today, we position portfolios to both weather potential volatility and capitalize on opportunities that may emerge. We appreciate your continued trust and remain focused on navigating the evolving market environment with prudence and clarity.

Warmest Regards,

Dr. Christian Koch, CFP®, CPWA®, CDFA®, RICP®